All Categories

Featured

Table of Contents

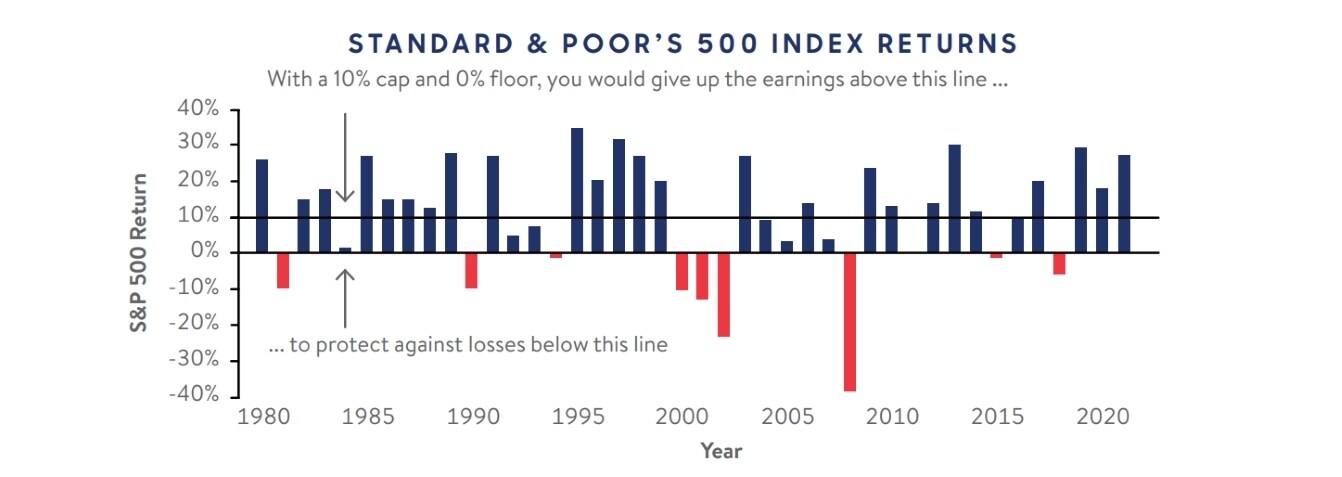

Below is a hypothetical contrast of historical efficiency of 401(K)/ S&P 500 and IUL. Allow's think Mr. SP and Mr. IUL both had $100,000 to saved at the end of 1997. Mr. SP spent his 401(K) money in S&P 500 index funds, while Mr. IUL's cash was the money worth in his IUL policy.

IUL's policy is 0 and the cap is 12%. After 15 years, at the end of the 2012, Mr. SP's profile expanded to. However because Mr. IUL never shed money in the bearish market, he would certainly have two times as much in his account Also better for Mr. IUL. Since his cash was conserved in a life insurance coverage policy, he does not need to pay tax obligation! Of program, life insurance policy safeguards the family and supplies sanctuary, foods, tuition and medical expenses when the insured passes away or is seriously ill.

Zap Co Iul

Life insurance policy pays a death advantage to your beneficiaries if you must die while the policy is in result. If your household would deal with economic hardship in the event of your fatality, life insurance coverage supplies peace of mind.

It's not one of the most lucrative life insurance policy financial investment plans, however it is among one of the most safe and secure. A type of permanent life insurance policy, global life insurance coverage allows you to pick just how much of your premium goes towards your survivor benefit and just how much goes into the policy to accumulate cash money worth.

In addition, IULs permit insurance policy holders to take out loans versus their policy's money worth without being taxed as earnings, though unsettled balances might undergo taxes and fines. The key benefit of an IUL policy is its potential for tax-deferred development. This implies that any type of revenues within the policy are not strained till they are taken out.

On the other hand, an IUL policy may not be the most ideal cost savings prepare for some individuals, and a conventional 401(k) could confirm to be much more advantageous. Indexed Universal Life Insurance Policy (IUL) policies use tax-deferred growth possibility, defense from market declines, and survivor benefit for beneficiaries. They permit insurance policy holders to earn passion based on the efficiency of a securities market index while safeguarding versus losses.

Iul Italian University Line

A 401(k) strategy is a prominent retired life cost savings choice that enables individuals to spend money pre-tax right into various financial investment devices such as common funds or ETFs. Employers might likewise offer matching payments, better enhancing your retirement cost savings possibility. There are 2 primary types of 401(k)s: typical and Roth. With a standard 401(k), you can decrease your gross income for the year by adding pre-tax bucks from your income, while also benefiting from tax-deferred development and employer matching payments.

Several employers additionally offer matching contributions, successfully giving you complimentary money towards your retired life strategy. Roth 401(k)s feature likewise to their traditional equivalents yet with one key distinction: taxes on payments are paid upfront instead of upon withdrawal during retirement years (iul sa). This suggests that if you anticipate to be in a greater tax brace during retirement, adding to a Roth account can save money on tax obligations over time compared to spending entirely through conventional accounts (resource)

With reduced administration charges usually contrasted to IULs, these types of accounts permit financiers to conserve cash over the lengthy term while still benefiting from tax-deferred growth potential. In addition, numerous preferred affordable index funds are readily available within these account types. Taking circulations prior to reaching age 59 from either an IUL plan's money worth via car loans or withdrawals from a conventional 401(k) strategy can result in adverse tax obligation ramifications otherwise handled meticulously: While obtaining versus your policy's cash money value is typically considered tax-free approximately the quantity paid in costs, any unsettled car loan balance at the time of death or plan surrender may go through earnings tax obligations and fines.

Indexed Universal Life Vs Roth Ira: Pros, Cons, And Retirement Strategies

A 401(k) gives pre-tax investments, company matching payments, and potentially even more investment selections. www iul com. Talk to a economic organizer to identify the finest choice for your scenario. The drawbacks of an IUL include greater management prices compared to standard retirement accounts, constraints in investment choices due to plan constraints, and possible caps on returns throughout solid market efficiencies.

While IUL insurance might show useful to some, it's important to understand just how it works before acquiring a plan. Indexed global life (IUL) insurance coverage policies provide better upside possible, versatility, and tax-free gains.

As the index moves up or down, so does the price of return on the cash money value component of your plan. The insurance policy business that provides the policy may use a minimal surefire rate of return.

Economists typically suggest having life insurance protection that amounts 10 to 15 times your yearly income. There are a number of disadvantages associated with IUL insurance coverage that movie critics are quick to aim out. For instance, someone that develops the policy over a time when the market is doing improperly might end up with high costs settlements that do not contribute whatsoever to the cash worth.

Apart from that, maintain in mind the adhering to various other factors to consider: Insurance provider can establish engagement prices for just how much of the index return you receive each year. Allow's say the policy has a 70% involvement rate. If the index grows by 10%, your money worth return would certainly be just 7% (10% x 70%)

Furthermore, returns on equity indexes are commonly topped at a maximum quantity. A plan might state your maximum return is 10% each year, regardless of exactly how well the index performs. These restrictions can restrict the real rate of return that's credited towards your account each year, regardless of just how well the policy's hidden index performs.

Iule

It's vital to consider your individual danger resistance and investment objectives to ensure that either one straightens with your overall strategy. Whole life insurance policy plans often consist of an assured rate of interest with foreseeable superior quantities throughout the life of the plan. IUL plans, on the other hand, offer returns based on an index and have variable premiums over time.

There are several other kinds of life insurance policies, clarified below. offers a fixed benefit if the policyholder dies within a collection amount of time, generally between 10 and 30 years. This is one of one of the most budget friendly types of life insurance coverage, along with the most basic, though there's no money value buildup.

Is Iul Good For Retirement

The plan acquires value according to a taken care of schedule, and there are less charges than an IUL policy. They do not come with the flexibility of adjusting costs. includes also more flexibility than IUL insurance policy, implying that it is also much more difficult. A variable plan's money value may depend on the efficiency of details stocks or other safety and securities, and your costs can likewise change.

{kind=link}

Latest Posts

Universal Life Insurance Calculator Cash Value

Universal Life Surrender Value

Universal Life Insurance For Retirement Income